Maxwell supports many cost strategies for each line of coverage:

- Medical

- Dental and vision

- Disability

- Basic life

- Critical illness and voluntary life

- Accident/hospital indemnity

- Cancer

Before we get started, please note that Maxwell does not support rates for long term care or worksite products, but they can be built as informational-only.

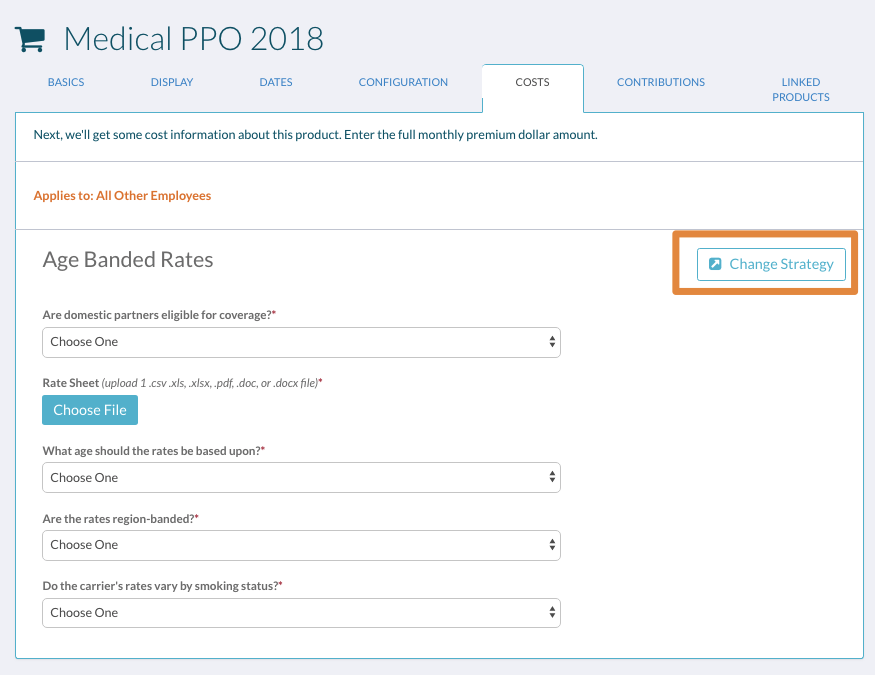

Medical Costs

Maxwell supports medical plans with the following cost strategies:

- Composite rates (2 tier, 3 tier or 4 tier)

- Age banded rates (individual or composite)

- Fixed dollar amount (i.e. flat rate)

If you're adding or renewing plans in Tempo, you’ll review the cost strategy on the “Costs” tab. You can also indicate if the rates vary based on smoking status (employee and/or spouse).

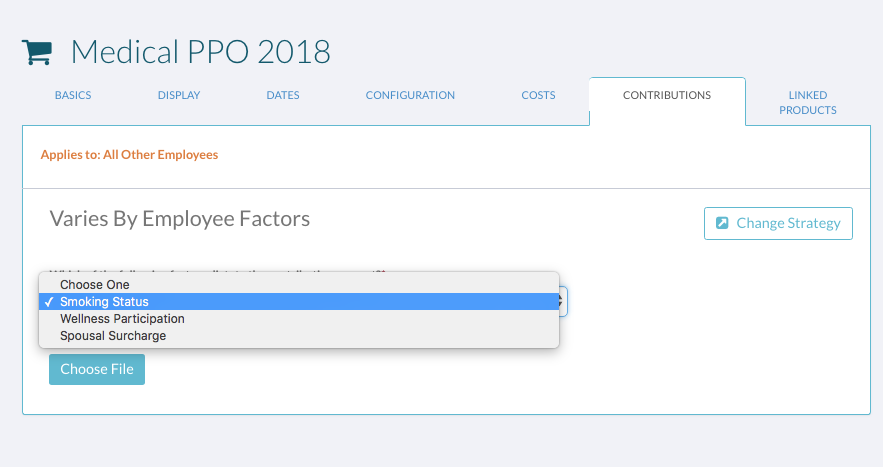

- You can also set up the employer’s contribution strategy to vary by employee factors including:

- Smoking status

- Wellness participation (employee and/or spouse)

- Spousal surcharge

- Maxwell also supports gender banded rates (both composite and age banded) if the plan is grandfathered into this rating structure. Please talk to your Implementation Team on how to get these rates uploaded into the portal.

- Maxwell does not support child smoking status rates that are based on the employee’s age.

- You can implement up to two employee factors on a given product.

| Need some examples? Check out this quick PDF that includes examples with detailed calculations for medical age-banded plans. |

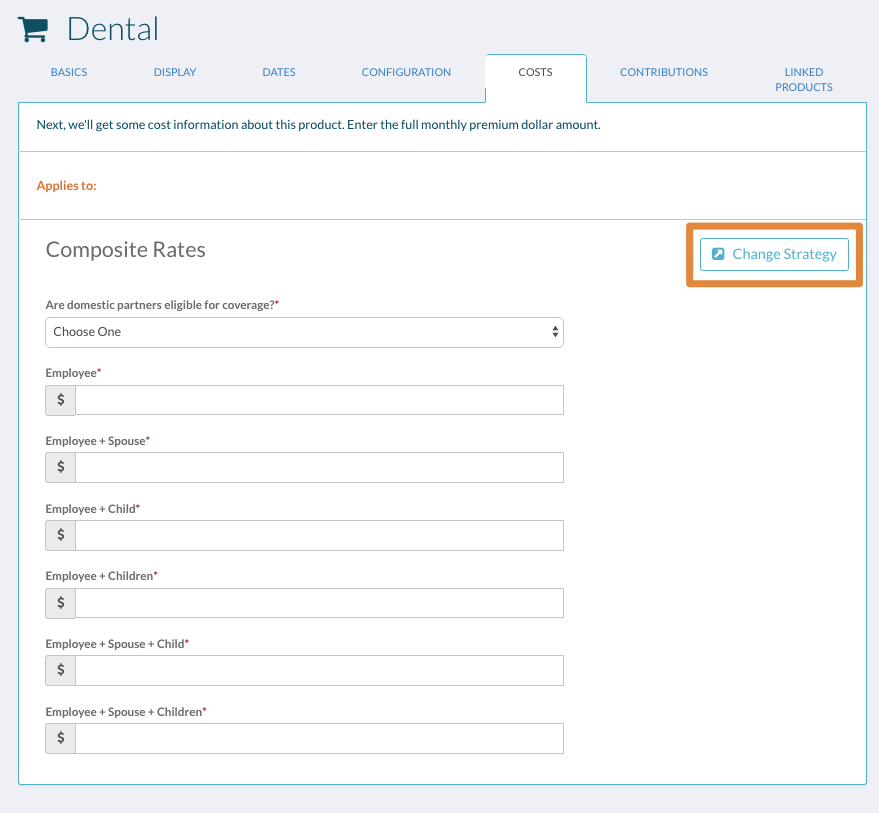

Dental/Vision Costs

Maxwell supports dental and vision plans with the following cost strategies:

- Composite rates (2 tier, 3 tier or 4 tier)

- Fixed dollar amount (i.e. flat rate)

If you're adding or renewing non-Sun Life plans in Tempo, you’ll review the cost strategy on the “Costs” tab.

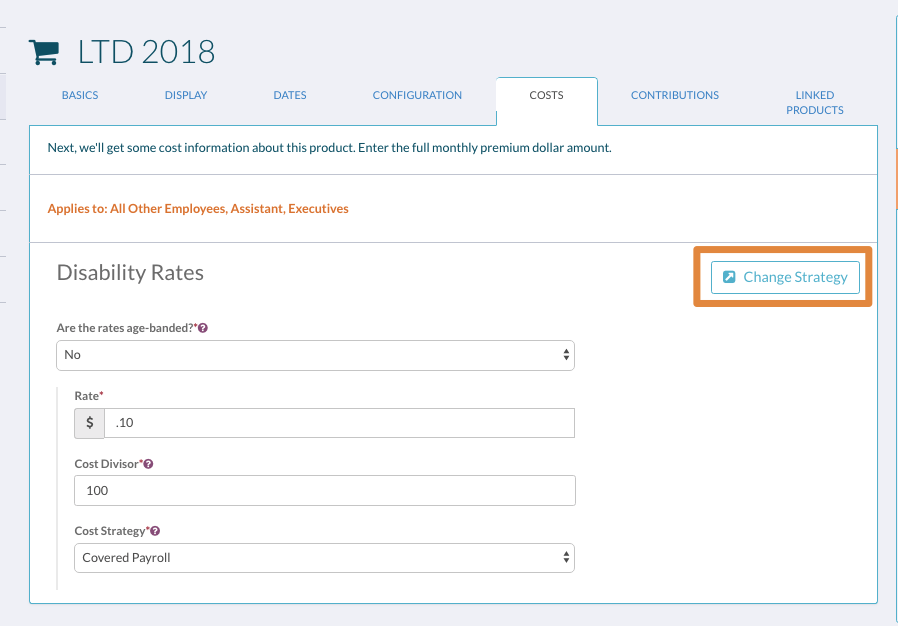

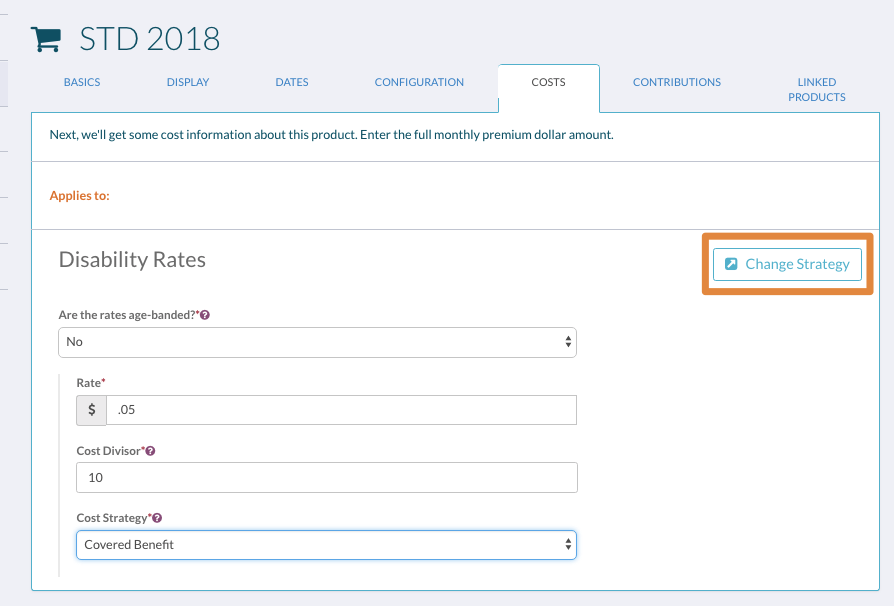

Disability Costs

Maxwell supports disability plans with the following cost strategies:

- Age banded

- Flat rate (example: $0.10 per $100 of covered payroll/covered benefit)

Covered Benefit vs. Covered Payroll

Covered Payroll: Cost is calculated based on covered monthly payroll.

- LTD plan example:

- $100,000 (employee’s salary)/12 (months in a year)= $8,333 (monthly payroll/salary)

- $8,333 (monthly payroll/salary)/100 (cost divisor)* $0.10 (cost per $100 of monthly salary)=$8.33 monthly premium cost

- $100,000 (employee’s salary)/12 (months in a year)= $8,333 (monthly payroll/salary)

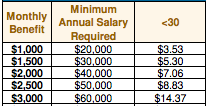

- STD plan example:

- $100,000 (employee’s salary)/52 (weeks in a year)= $1,923 (weekly salary)

- $1,923 (weekly salary)*0.6 (benefit %)= $1,154 (weekly benefit))/10 (cost divisor)*$0.05 (cost per $10 of weekly benefit)= $5.77 monthly premium cost

- $100,000 (employee’s salary)/52 (weeks in a year)= $1,923 (weekly salary)

| Need some examples? Check out this quick PDF that includes examples with detailed calculations for LTD and STD plans. |

- Maxwell also supports rating by tax choice. Please talk to your Implementation Team on how to get these rates uploaded into the portal.

- Maxwell does not support non-linear rates on disability plans. Here’s an example of this type of rating strategy:

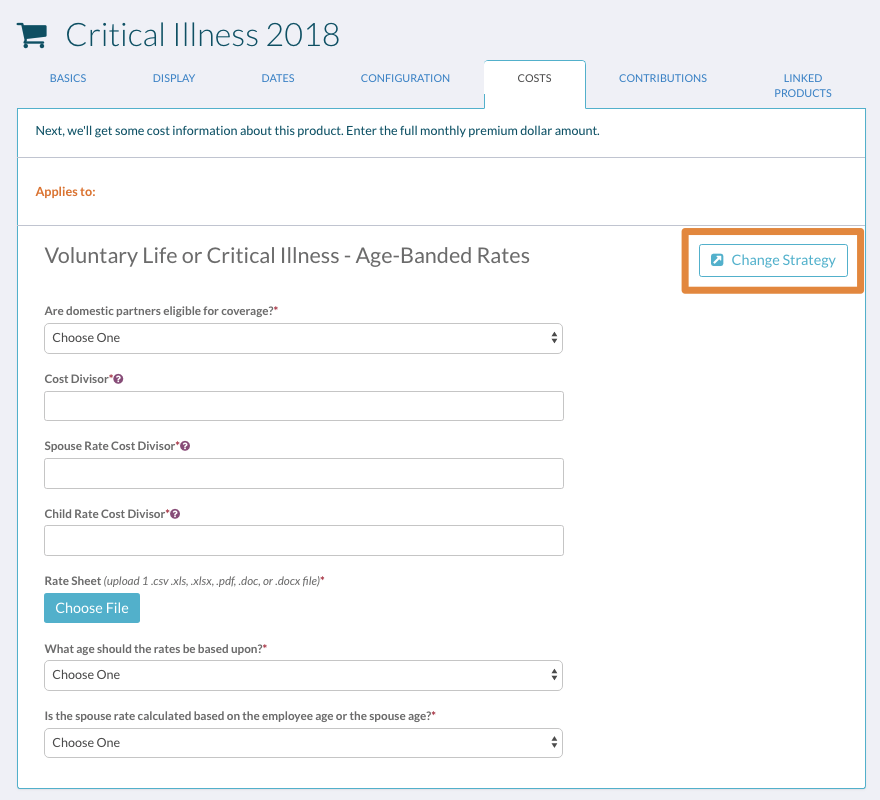

Critical Illness / Voluntary Life Costs

Maxwell supports critical illness and voluntary life plans with the following cost strategies:

- Composite rates (2 tier, 3 tier or 4 tier)

- Age banded rates (individual or composite)

If you're adding or renewing non-Sun Life plans in Tempo, you’ll review the cost strategy on the “Costs” tab. Here, you can also indicate if the rates vary based on smoking status (employee and/or spouse).

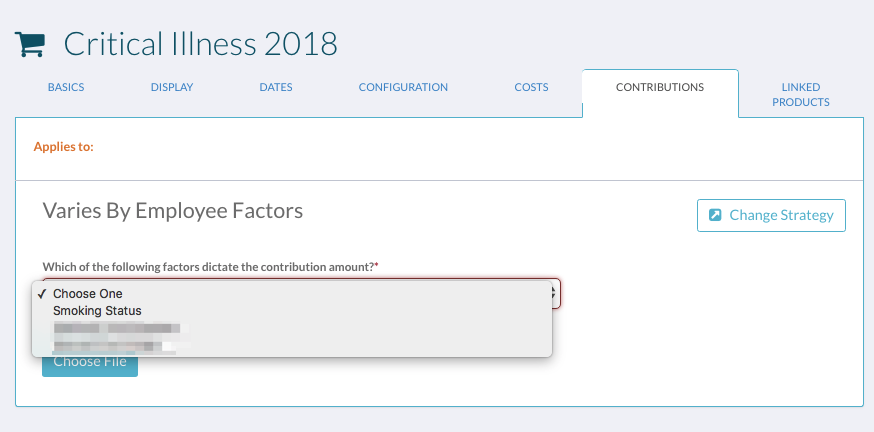

- You can also set up the employer’s contribution strategy to vary by smoking status (employee and/or spouse) on critical illness plans.

- Other complex rates are supported on a case-by-case basis depending on the complexity. The Implementation Team can review and let you know if the strategy is supported.

- Maxwell does not support child smoking status rates that are based on the employee’s age.

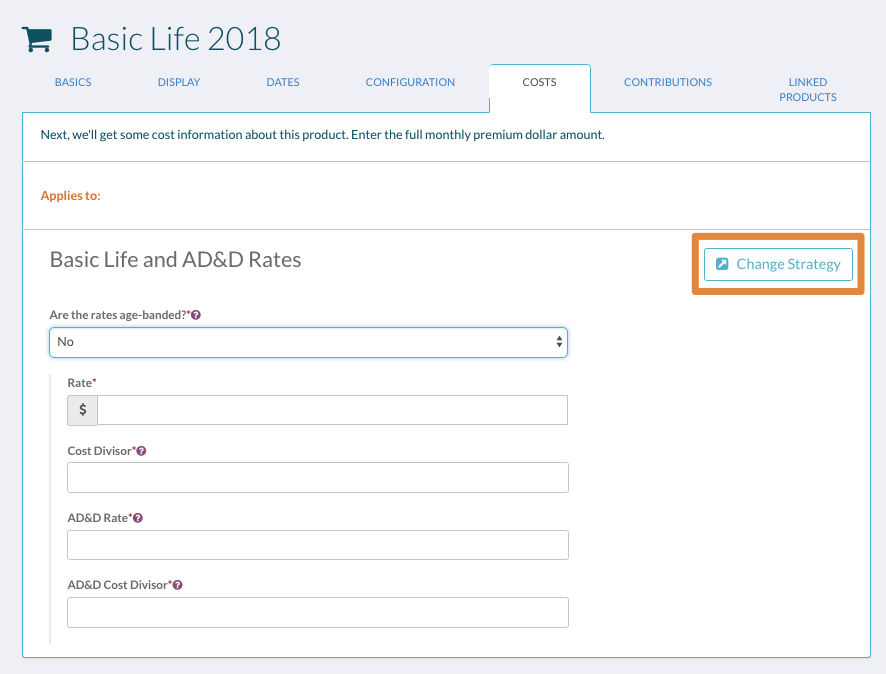

Basic Life Costs

Maxwell supports basic life plans with the following cost strategies:

- Age banded rates

- Flat rate (i.e. fixed dollar amount)

If you're adding or renewing non-Sun Life plans in Tempo, you’ll review the cost strategy on the “Costs” tab.

Learn more about the term life plan structures that are supported here.

| Need some examples? Check out this quick PDF that includes examples with detailed calculations for Basic Life, Voluntary Life and AD&D. |

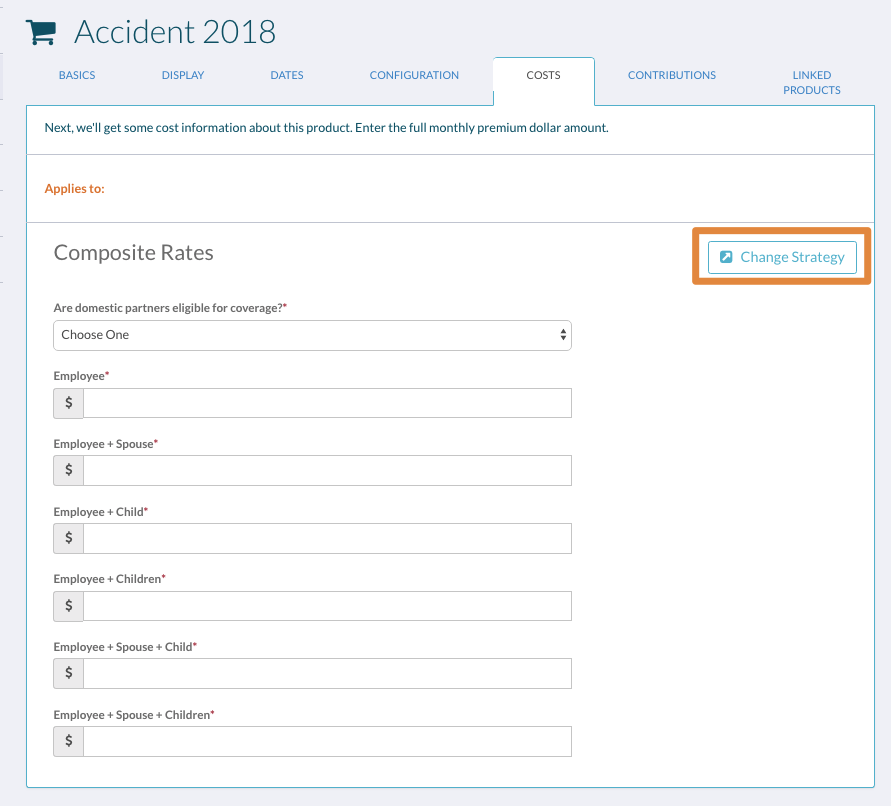

Accident/Hospital Indemnity Costs

Maxwell supports accident and hospital indemnity plans with the following cost strategies:

- Composite rates (2 tier, 3 tier or 4 tier)

- Age banded rates (individual or composite)

If you're adding or renewing non-Sun Life plans in Tempo, you’ll review the cost strategy on the “Costs” tab.

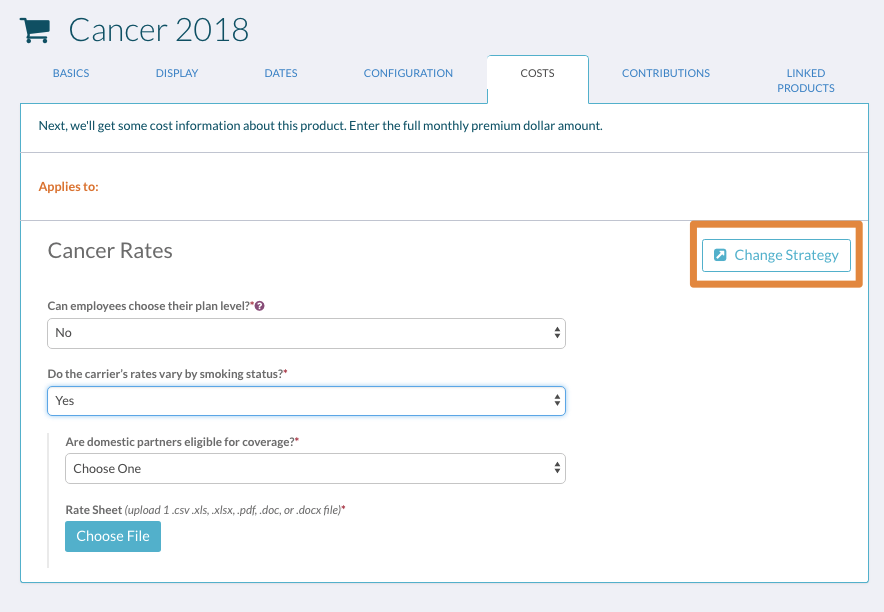

Cancer Costs

Maxwell supports cancer plans with the following cost strategies:

- Composite rates (2 tier, 3 tier or 4 tier)

- Age banded rates (individual or composite)

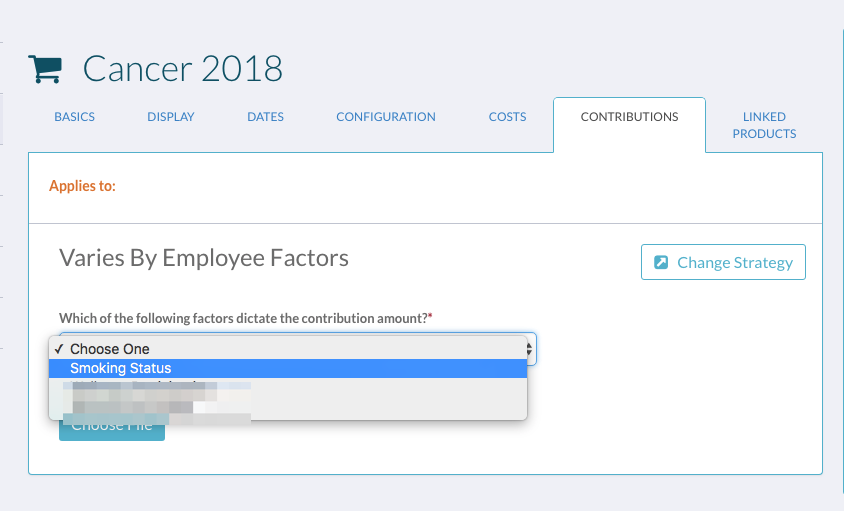

Employee factors: Maxwell supports rates by smoking status (employee and/or spouse) on cancer plans.

If you're adding or renewing non-Sun Life plans in Tempo, you’ll review the cost strategy on the “Costs” tab. Here, you can also indicate if the rates vary based on smoking status (employee and/or spouse).

Note: You can also set up the employer’s contribution strategy to vary by smoking status (employee and/or spouse) on cancer plans.

General note on plans with age banded rates