In this article:

What is evidence of insurability?

How does Maxwell handle evidence of insurability?

Are there any exceptions?

What else should I be aware of?

What is evidence of insurability?

Evidence of insurability (EOI) is personal health information that insurance carriers require plan participants to provide. This is often done through an EOI application that serves as a medical questionnaire.

Carriers usually request an EOI application to be submitted for voluntary plans when the plan participant chooses a coverage amount that is over the guaranteed issue amount (the amount of coverage that is pre-approved by the carrier).

The carrier will also require EOI if the plan participant:

- Chooses to enroll in any amount of coverage when they declined coverage in the past

- Chooses to increase their existing coverage by any amount

These are commonly known as late entry rules (or late entry penalties). They’re a standard way for carriers to manage their risk for voluntary plans.

How does Maxwell handle evidence of insurability?

Here’s what happens in Maxwell if an employee, spouse, or child elects coverage in a plan that requires EOI based on the above rules:

- Employee enrolls in the benefit

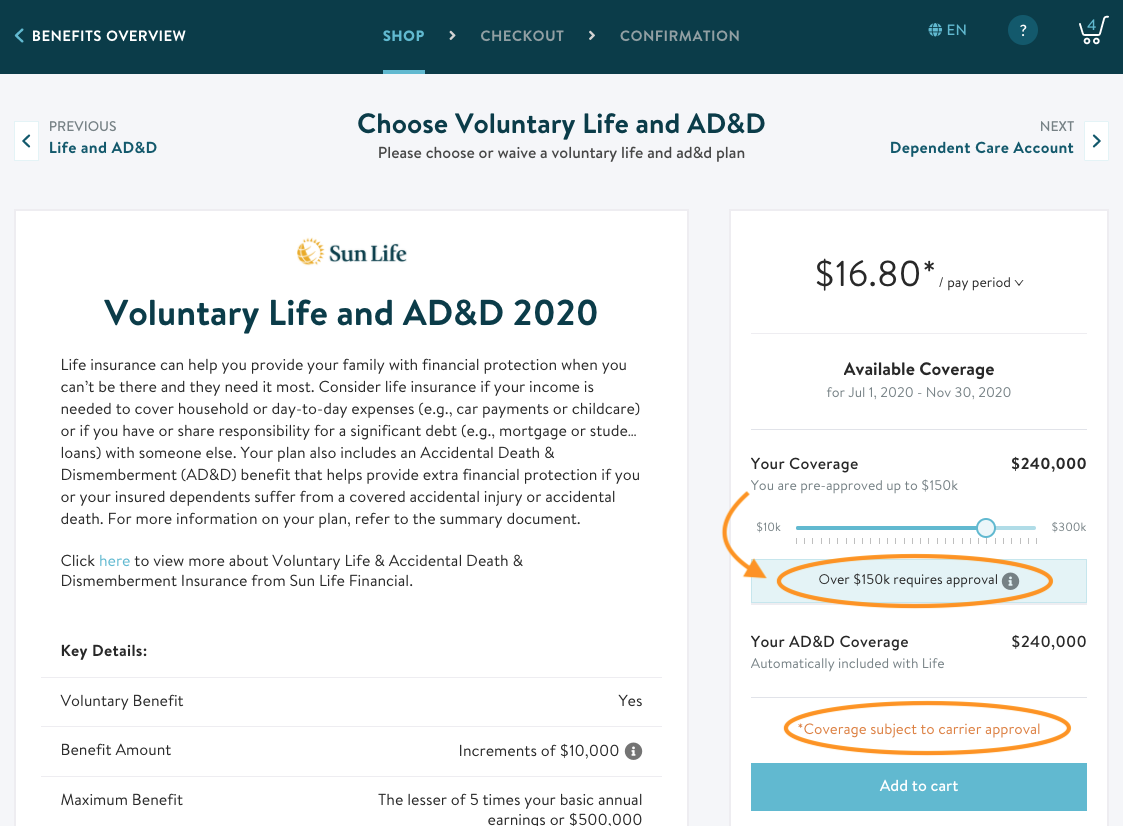

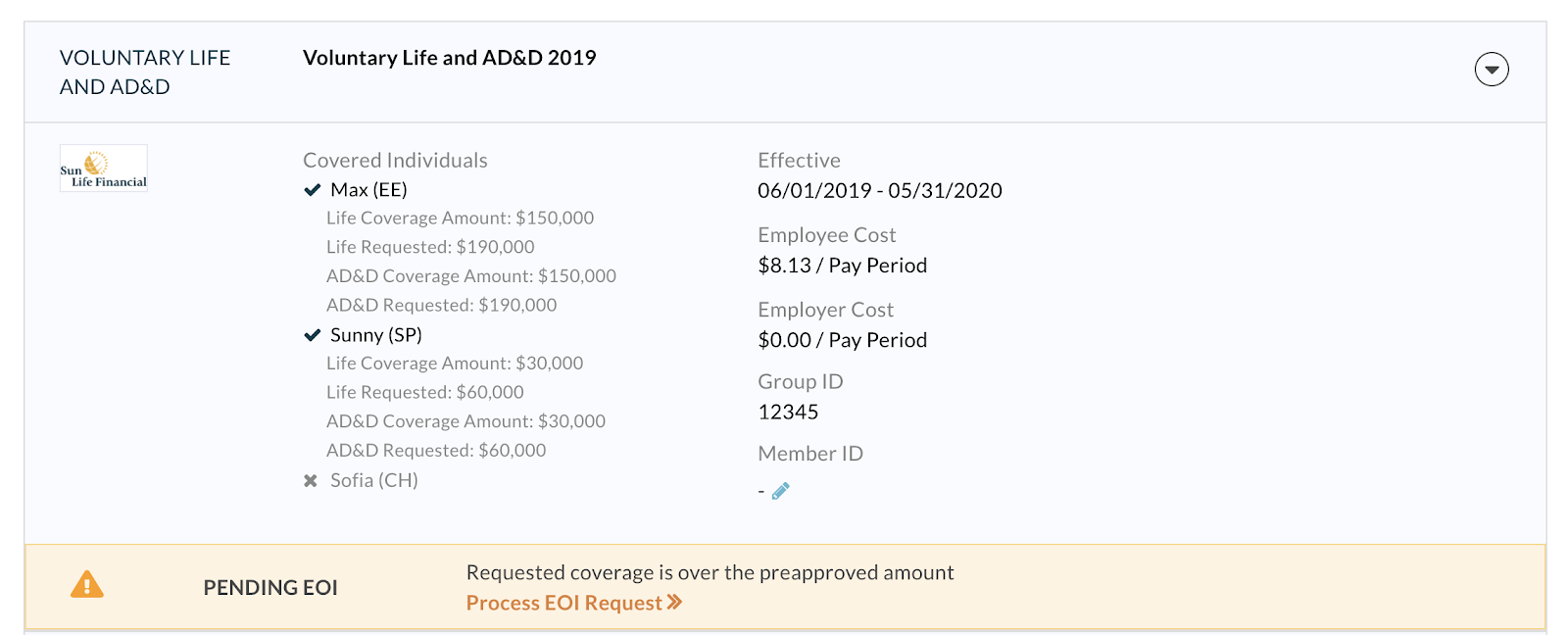

They’ll see their pre-approved amount and their pending amount represented once they enter a coverage amount over their guaranteed issue:

If you’re ever electing coverage on behalf of the employee in Maxwell, you should add the entire coverage amount that the employee would like to elect on the voluntary plan. The system will automatically let you know what coverage is pre-approved and what coverage is pending EOI.

-

You review the enrollment

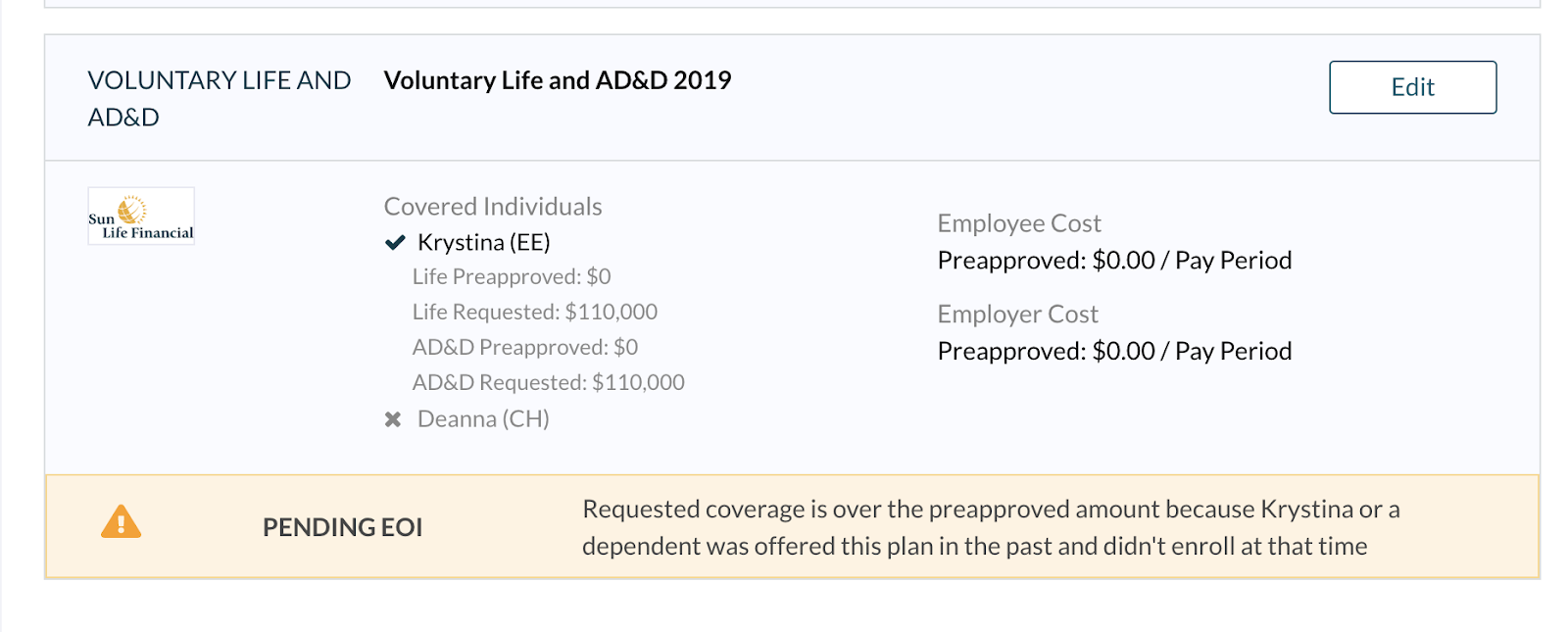

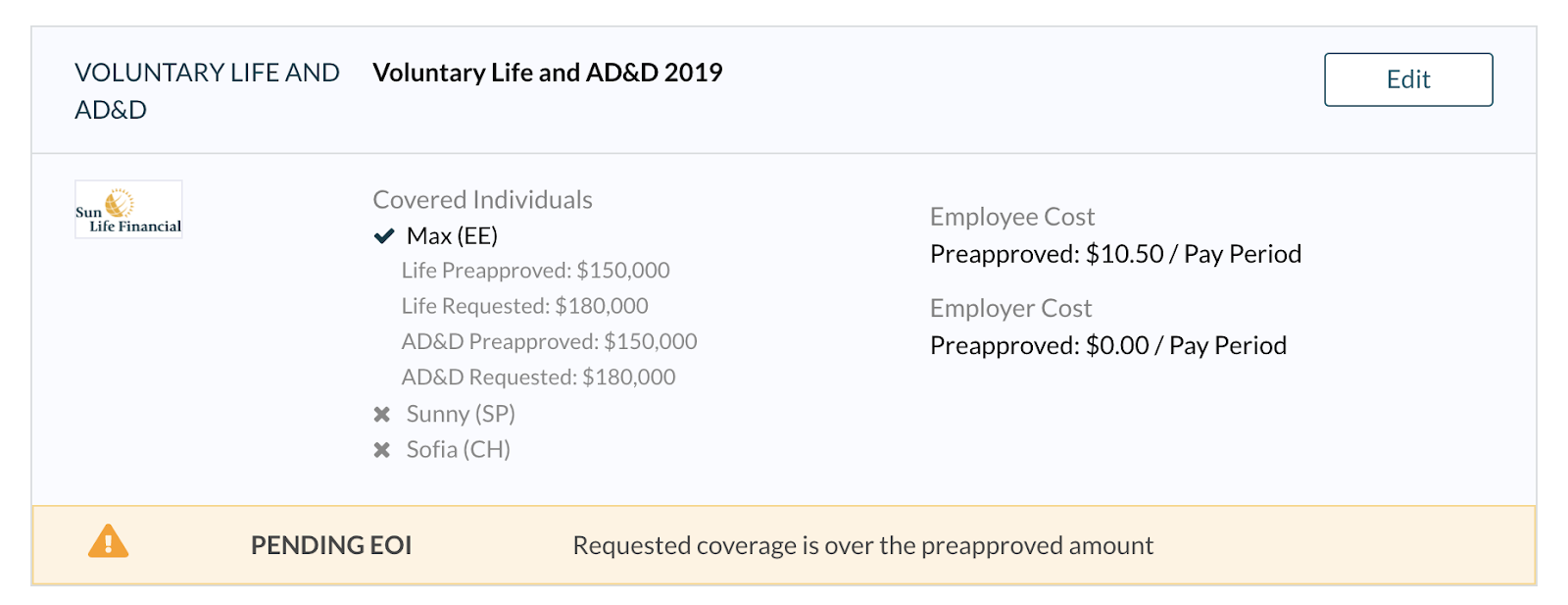

As the Administrator, if you view the event details on the employee’s profile, you’ll see that the employee has elected the voluntary plan and that the coverage is pending EOI. You can also tell the reason that EOI was needed—either the coverage amount was over the guaranteed issue, or if the plan participant is a late entrant into the plan.

If the employee is in OE and you want to see if an election they’ve made requires EOI before you’ve ended the event, go to the employee’s profile and click Actions > View Event Details on the banner. You can then see if the election they made is pending EOI by going to the “Benefits” section.

Whether it’s an open enrollment event, a new hire event, or a life event, you’ll approve the pre-approved amounts by approving and ending the event. You can then view the pre-approved coverage and the total amount requested on the employee’s “Benefits” tab:

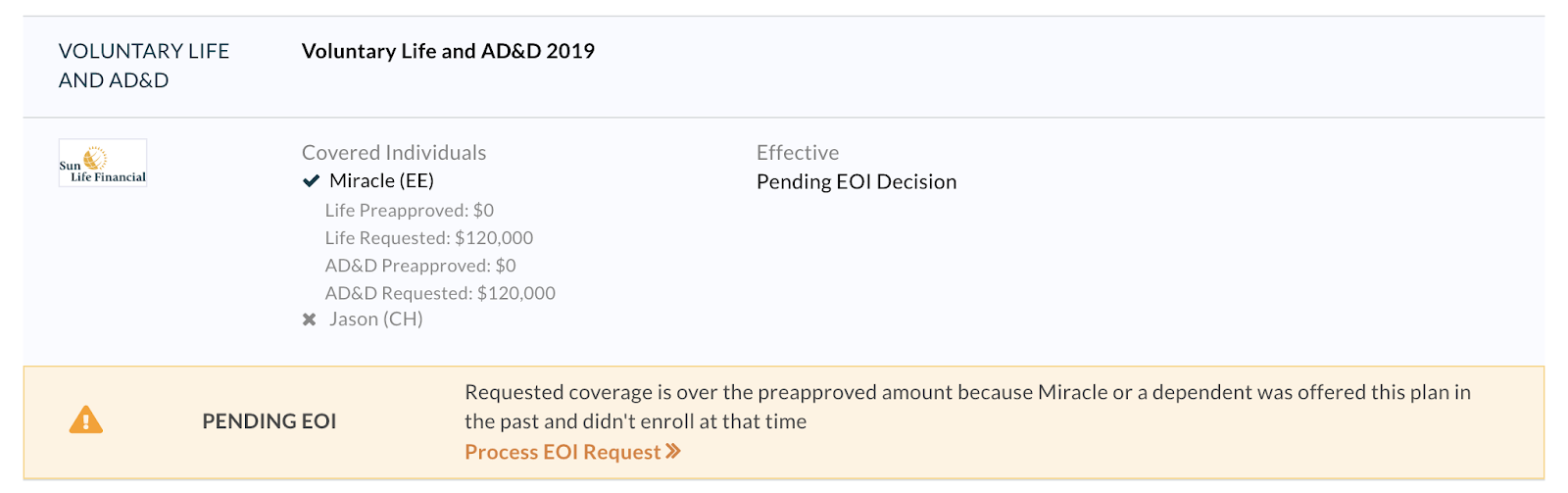

For plans that are pending EOI due to late entry with a pre-approved amount is $0, the cost will be hidden, and the effective date will be listed as “Pending EOI Decision.”

Please Note: For any clients with non Sun Life voluntary benefits, you may see the words "Process EOI Request" on the pre-approved coverage that you can view on the employee's Benefits tab. This is because you will have to process the remaining, pending coverage amount once you hear back from the non Sun Life carrier on whether the pending amount was approved or denied. Learn more here.

Sun Life voluntary benefits are automatically processed once the pending EOI amount is approved, which means that you will not have to process the remaining approved volume in the portal.

For an annual Open Enrollment, you can also download a report that will list all the enrollments that were part of the OE and include coverage that’s pending EOI. This report will be available right on the screen after you end the OE.

- Employee completes the EOI application

Within two business days of submitting their enrollment, any employee with a pending Sun Life EOI amount will receive an email with instructions prompting them to complete their EOI application. These employees will also receive reminder emails 15 days, 25 days, and 80 days after the first email is sent if they still haven't completed the application. For any client with a non Sun Life pending EOI amount, the employee will need to fill out the carrier's EOI application. How this is done depends on the carrier, so you'll want to look up the process on the carrier's website or contact your carrier's representative.- If you have EOI forms set up in your portal: Maxwell will immediately send the employee an EOI form to complete when they submit their enrollment. Learn more about auto-sending forms here >

- If you have EOI forms set up in your portal: Maxwell will immediately send the employee an EOI form to complete when they submit their enrollment. Learn more about auto-sending forms here >

- You send the elections over to the carrier

-

- If you have a Sun Life benefit, you do not need to take this step as Sun Life will have the coverage information right away. You do not need to approve the EOI request in Sun Life Connect to start the application review process.

- If you have an EDI connection with the carrier, this will happen automatically. Please note that the election may send over to the carrier before you approve the event.

- If you're using forms, you should send the completed EOI forms over to the carrier.

- If you're using Maxwell reports, you'll want to run the “Pending Elections Report” which will always display the full requested coverage amount, even if the pre-approved amounts have already been approved (by ending the event). The pre-approved amounts that have been processed will display on the “Coverage Report.” Similarly, the “Pending Elections Cost Report” will show cost information based on the full requested coverage amount, even if the pre-approved amounts have already been processed. The cost of the pre-approved amounts will display on the “Enrolled Cost Report.”You send the elections over to the carrierThe carrier reviews the elections and the employee's application

You can track the EOI application status within Sun Life Connect.

-

- The carrier notifies you that the additional coverage amounts are approved or denied

Sun Life will communicate the decision to you via email, but you do not need to take any action in Maxwell. The decision will be processed in Maxwell on your behalf. Sun Life will also communicate their decision to the employee directly via email and postal mail for approvals, and via postal mail only for denials.

Are there any exceptions to the above rules?

Special rules during annual open enrollment

In an effort to increase participation, some carriers may offer different evidence of insurability requirements during your company’s annual open enrollment. While a carrier will always require evidence of insurability for employees who are offered the product for the first time and choose to elect over the guaranteed issue, they may allow some flexibility when it comes to those who were previously offered coverage or want to increase their coverage at this point.

Maxwell offers the flexibility to run an open enrollment that allows every employee and spouse to be treated as a first-time enrollee with access to the guaranteed issue, regardless of their past interactions with the product (sometimes called a “true open enrollment” or “one-off special open enrollment”).

Maxwell also offers the ability to enable employees to increase their inforce coverage by an additional amount without requiring evidence of insurability (sometimes called “additional purchase guarantee” or “one-off provision”).

Your Implementation Consultant will set this up in your Maxwell portal during implementation if you let us know the carrier offers these terms during portal set up.

Special Rules Outside of Open Enrollment

-

- If an effort to increase participation, some carriers may allow late entrants to enroll in the lowest increment without requiring evidence of insurability. This is an available option for any plans with late entry rules, as long as the plan allows employees to choose their increment amounts. This will be set up in your Maxwell portal if the carrier offers these terms.

- Some carriers may also allow late entrants to enroll up to the guaranteed issue amount without requiring evidence of insurability for certain life events that result in a family status change, including: Birth or Adoption of a Child, Change in Domestic Partnership Status, Change to Spouse Coverage, Family and Medical Leave Act, Marriage, Divorce, Death of Spouse or Dependent, Part-time to Full-time, Full-time to Part-time, Spouse Loss/ Gain Insurance Eligibility.

- Note: If this rule is not set up, EOI will be required during any life event for the employee or spouse (other than Marriage and Change in Domestic Partnership Status for the spouse).

Special rules for rehires

At times, carriers allow rehires not to be subject to EOI based on late entry rules if it’s been an extended period of time since they left the company and were previously enrolled in or offered coverage. Currently, Maxwell does not allow for this scenario and ensures late entry rules are applied to all rehires, regardless of how long it’s been since they were previously employed by the company. (Of course, this requires that the employee was listed in the Maxwell system during their previous employment). While this may cause a voluntary product to pend EOI when it’s not necessary, the Administrator can always manually approve the full amount in Maxwell without having the individual complete a form.

What else should I be aware of when it comes to evidence of insurability?

- In Maxwell, evidence of insurability can be set up on all voluntary lines of coverage (life, critical illness, disability) except for voluntary cancer and voluntary accident plans. EOI is not commonly covered for these types of plans.

- Maxwell does not support giving late entrants access to a guaranteed issue amount above $0.

- One of the late entry rules mentioned above is if an employee declines coverage, they will be subject to evidence of insurability the next time they’re offered coverage. Please note that in the Maxwell platform, the employee does not need to actively waive or even log in to be considered as “declining” coverage. They only need to have been offered the product at a point in time.

- For voluntary critical illness products, some carriers do not use a form and instead have the employee answer health questions right in the Maxwell shopping experience after they elect a coverage amount that requires EOI. For those products, Maxwell does not currently support late entry rules and only requires EOI if the employee elects over the guaranteed issue. You can manually administer late entry for these products by following these steps.