This article reviews:

- How per pay period amounts are calculated in Maxwell

- Where per pay period amounts are displayed in Maxwell

- Important notes about cost calculations in Maxwell

How per pay period amounts are calculated in Maxwell

In Maxwell, per pay period amounts are calculated in different ways, depending on the pay frequency, whether the product has a monthly premium or annual contribution, and whether you have pay dates entered into Maxwell.

Please note: If paycheck dates are entered in your payroll calendar, Maxwell will use the dates to calculate per pay period deduction amounts for employees. In that case, Maxwell counts the number of pay dates entered from the employee's product effective date until the employee's product end date.

If your benefits offering includes financial products with annual contributions, we recommend adding your payroll calendar to Maxwell for the most accurate calculations.

Monthly

- For products with a monthly premium: Same as the monthly premium.

- For products with an annual contribution: Maxwell divides the annual contribution by the number of remaining pay periods left in the plan year.

- If pay dates are entered into the Payroll Calendar: Maxwell counts the number of pay dates entered from the employee's product effective date until the employee's product end date.

- If pay dates are not entered into the Payroll Calendar: Maxwell assumes that your pay date is the last day of the month. The first pay date counted is the first one on or after the employee’s product effective date. Maxwell then counts the number of last days of the month prior to the employee’s product end date.

- Full plan year example: Jim Halpert renews an FSA product effective 1/1/20-12/31/20, contributing $1,000 annually. Per Maxwell's assumed schedule, there are 12 pay periods in the plan year. His per pay period amount is $83.33 (1,000/12).

- Mid plan year example: Jim Halpert is hired on 5/1/2020 and elects to contribute an annual amount of $1,000 towards an FSA product that has a plan year of 1/1/2020 - 12/31/2020. Per Maxwell's assumed schedule, there are 8 remaining pay dates from 5/1/2020 to 12/31/2020. So Jim's per pay period amount is $125 (1,000/8).

Semimonthly

- For products with a monthly premium: Maxwell takes the monthly premium and annualizes it by multiplying by 12. It then divides that number by 24.

- For products with an annual contribution: Maxwell divides the annual contribution by the number of remaining pay periods left in the plan year. The calculation of the number of pay periods remaining will depend on on whether pay dates are entered for the entire plan year.

- If pay dates are entered into the Payroll Calendar: Maxwell counts the number of pay dates entered from the employee's product effective date until the employee's product end date.

- If pay dates are not entered into the Payroll Calendar: Maxwell assumes that your pay dates are on the 15th and the last day of the month. The first pay date counted is the first one on or after the employee’s effective date. Maxwell then counts the number of 15ths and last days of the month prior to the employee’s product end date.

- Full plan year example: Jim Halpert renews an FSA product effective 1/1/20-12/31/20, contributing $1,000 annually. Per Maxwell's assumed schedule, there are 24 pay periods in the plan year. His per pay period amount is $41.67 (1,000/24).

- Mid plan year example: Jim Halpert is hired on 5/1/2020 and elects to contribute an annual amount of $1,000 towards an FSA product that has a plan year of 1/1/2020 - 12/31/2020. Per Maxwell's assumed schedule, there are 16 remaining pay dates from 5/1/2020 to 12/31/2020. So Jim's per pay period amount is $62.50 (1,000/16).

Biweekly

- For products with a monthly premium: Maxwell takes the monthly premium and annualizes it by multiplying by 12. It then divides that number by 26.

- For products with an annual contribution: Maxwell divides the annual contribution by the number of remaining pay periods left in the plan year. The calculation of the number of pay periods remaining will depend on on whether paycheck dates are entered for the entire plan year.

- If paycheck dates are entered into the Payroll Calendar: Maxwell counts the number of paycheck dates entered from the employee’s product effective date until the employee’s product end date.

- If paycheck dates are not entered into the Payroll Calendar: Maxwell assumes the payroll calendar by taking the product effective date, adding 14 calendar days to come up with the first pay date, then an additional 14 days to come up with the second pay date, and so on, until the end of the plan year. The first pay date counted is the first one after the employee's effective date. Maxwell then counts the number of pay dates prior to the employee's product end date.

- Full plan year example: Jim Halpert renews an FSA product effective 1/1/20-12/31/20, contributing $1,000 annually. Per Maxwell’s assumed schedule, there are 26 pay periods in the plan year. His per pay period amount is $38.46 (1,000/26).

- Mid plan year example: Jim Halpert is hired on 5/1/2020 and elects to contribute an annual amount of $1,000 towards an FSA product that has a plan year of 1/1/2020-12/31/2020. Per Maxwell’s assumed schedule, there are 18 remaining paycheck dates from 5/1/2020 to 12/31/2020. So Jim’s per pay period amount is $55.56 ($1,000/18).

Weekly

- For products with a monthly premium: Maxwell takes the monthly premium and annualizes it by multiplying by 12. It then divides that number by 52.

- For products with an annual contribution: Maxwell divides the annual contribution by the number of remaining pay periods left in the plan year. The calculation of the number of pay periods remaining will depend on on whether paycheck dates are entered for the entire plan year.

- If paycheck dates are entered into the Payroll Calendar: Maxwell counts the number of pay dates entered from the employee’s product effective date until the the employee’s product end date.

- If paycheck dates are not entered into the Payroll Calendar: Maxwell assumes the payroll calendar by taking the product effective date, adding 7 calendar days to come up with the first pay date, then an additional 7 days to come up with the second pay date, and so on, until the end of the plan year. The first pay date counted is the first one after the employee's effective date. Maxwell then counts the number of pay dates prior to the employee's product end date.

- Full plan year example: Jim Halpert renews an FSA product effective 1/1/20-12/31/20, contributing $1,000 annually. Per Maxwell’s assumed schedule, there are 52 pay periods in the plan year. His per pay period amount is $19.23 (1,000/52).

- Mid plan year example: Jim Halpert is hired on 5/1/2020 and elects to contribute an annual amount of $1,000 towards an FSA product that has a plan year of 1/1/2020-12/31/2020. Per Maxwell’s assumed schedule, there are 34 remaining paycheck dates from 5/1/2020 to 12/31/2020. So Jim’s per pay period amount is $29.42 ($1,000/34).

Proration

For HSA products, you can choose to have the employer contribution prorated. You can contact our Support Team if you want to set this up. When proration is enabled, the employee will only receive a portion of the annual employer contribution proportional to the number of pay periods enrolled out of the total number of pay periods in the plan year.

Example:

Jim Halpert is hired on 5/15/20 and is paid biweekly

His employer contributes $1,000 towards an HSA product with a plan year of 1/1/20 - 12/31/20

There are 16 pay dates remaining in the plan year

The employer contributes a prorated annual amount of $615.38 (1,000x(16/26)) over the remaining 16 pay periods

The employer per pay period contribution is $38.46 (615.38/16)

You should only choose this option if you have paycheck dates entered into Maxwell. If paycheck dates are not entered, Maxwell will use an assumed payroll schedule to prorate the amount.

Where per pay period amounts are displayed in Maxwell

Per pay period amounts show up in multiple places in the Maxwell platform, including Administrative reports, data connection files, and the employee experience.

Administrative Reports

Use the Enrolled Cost Report or Change Report to pull per pay period amount information for each product. You can also use the View Payroll Changes feature and associated report.

Data Connection Files

Per pay period amounts are also included in the cost information Maxwell sends over to third party vendors via EDI feeds as well as the following payroll and financial product data connections:

- Discovery Benefits integration

- Paylocity 180° File Sync

- Paylocity 360° API Integration

- ADP Workforce Now API integration

- ADP Workforce Now compatible payroll report

- Paycheck Flex Enterprise compatible payroll report

Administrator Experience

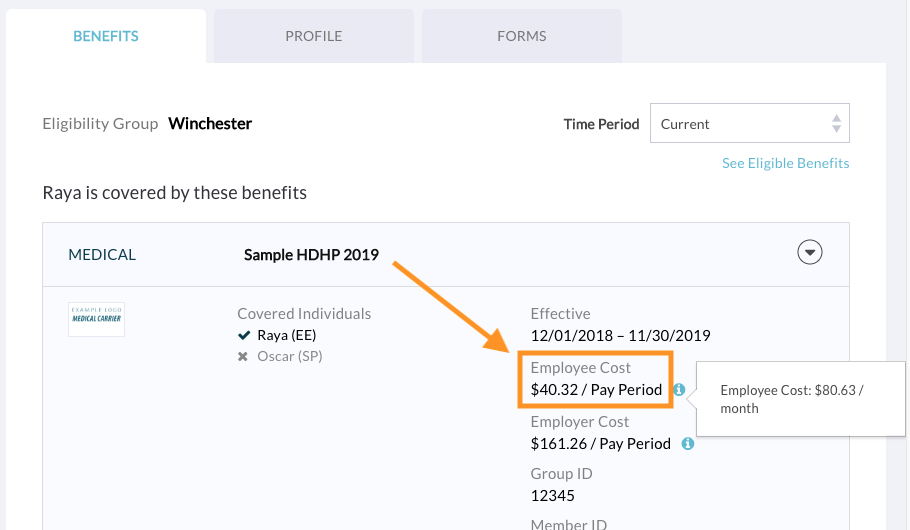

In addition to reports and files, per pay period amounts display in the HR Administrator experience in the employee's profile on the Benefits tab.

Employee Experience

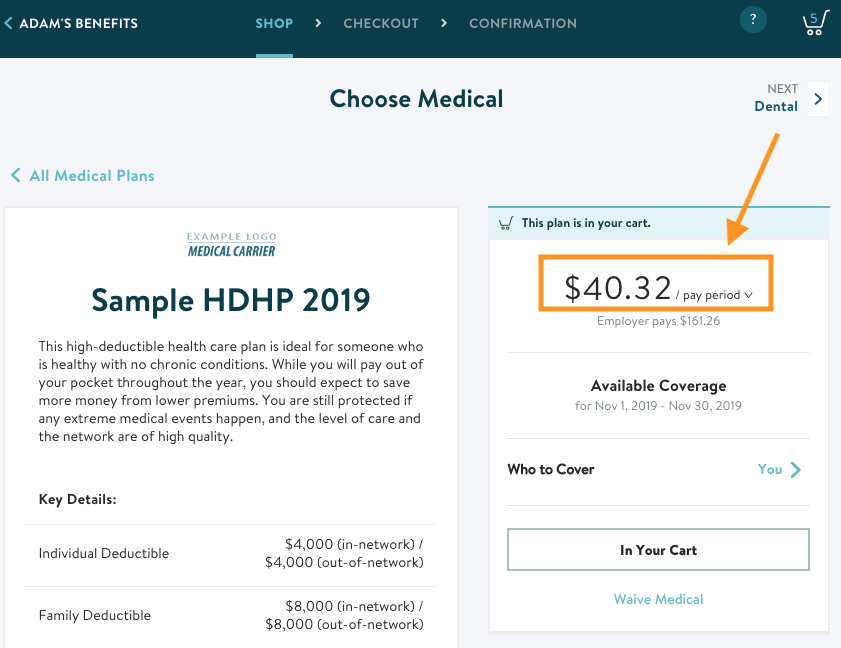

Maxwell displays per pay period amounts to employees during the shopping experience and after they enroll in benefits.

Important notes about cost calculations in Maxwell

We aim to provide the most accurate cost information possible, but there are a few limitations.

There are certain elements of per pay period amount calculations that Maxwell Health does not support and relies on the payroll vendor to accommodate.

Maxwell assumes that per pay period amounts are always counted during the product’s coverage period. Any adjustments to this (including payroll cut-off for new hires, premiums paid in advance, or premiums paid in arrears) will need to be adjusted manually outside of Maxwell. This also includes any one-time adjustments, including one-time deductions or any per pay period amounts that need to be prorated or retroactively adjusted.

- Ex: Jim Halpert is hired on March 14 and his benefits are effective on his DOH. According to his company’s payroll schedule, the next paycheck is March 15. Maxwell always assumes the benefits start getting deducted from the first paycheck following DOH. This means Maxwell assumes the first deduction will come out of his March 15 paycheck, even if per your company’s policy he did not meet the payroll cut-off.

Additionally, the following are not part of the cost calculations in the Maxwell platform:

- Imputed income (tax added to life benefits exceeding $50,000)

- Maxwell does not force federal and state taxation laws. The only tax option is set on the product during implementation, indicating whether the cost is pre- or post-tax.

- This includes the differential treatment of same sex taxation/benefits, which are especially complex due to the extraordinarily complex provisions around taxation of domestic partner benefits. These provisions can vary greatly depending on same versus opposite sex, federal versus state, as well as what the vendor has decided is allowable for the specific plan. As a result, Maxwell Health does not serve as the system of record for taxes. In our experience, the payroll administrator drives taxation treatment, most often via deduction codes, and is best suited to handle this for the employer.

- This includes the differential treatment of same sex taxation/benefits, which are especially complex due to the extraordinarily complex provisions around taxation of domestic partner benefits. These provisions can vary greatly depending on same versus opposite sex, federal versus state, as well as what the vendor has decided is allowable for the specific plan. As a result, Maxwell Health does not serve as the system of record for taxes. In our experience, the payroll administrator drives taxation treatment, most often via deduction codes, and is best suited to handle this for the employer.

- Earnings adjustments. For example, if you choose to add the cost of any plan premium to the employee’s salary, we cannot reflect this cost in Maxwell.

- Any surtax